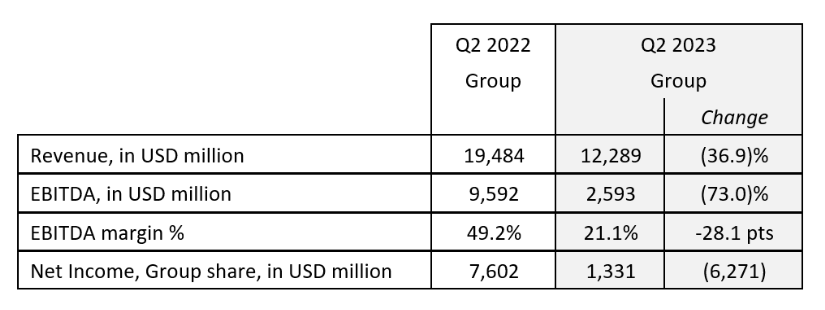

A.P. Moller – Maersk reports a second quarter of 2023 ahead of expectations with revenue standing at US$13 billion, compared to US$21.7 billion in the same quarter last year.

Ocean revenue decreased to US$8.7 billion, driven by a decrease in freight rates and loaded volumes. The company noted that while the volume and rate environment stabilised at a lower level during the second quarter, Ocean sector continued to be impacted by lower demand, driven by a significant inventory correction in particular in North America and Europe.

Furthermore, revenue in Logistics & Services was US$3.4 billion with the sector being impacted by lower volumes due to the continued destocking and weaker consumer demand, as well as low rates.

Moreover, revenue in Terminals decreased to US$950 million, influenced by the normalisation of storage revenue and lower volumes amid lower consumer demand and less congestion in North America.

Revenue

| USD million | 2023 Q2 | 2022 Q2 |

| Ocean |

8,703

|

17,412

|

| Logistics & Services |

3,386

|

3,502

|

| Terminals |

950

|

1,124

|

| Towage & Maritime Services |

504

|

579

|

| Unallocated activities, eliminations, etc. |

-555

|

-967

|

| A.P. Moller – Maersk consolidated |

12,988

|

21,650

|

“The ongoing market normalisation continued through the quarter leading to lower volumes and lower rates,” said the Danish carrier, which raised its financial outlook for the year, expecting now underlying EBITDA of US$9.5 – 11 billion and underlying EBIT of US$3.5 – 5 billion despite a weakened second half market outlook.

| Guidance | |

|---|---|

|

EBITDA Underlying

(Previously: 8.0-11.0) |

US$9.5-11 billion

|

|

EBIT Underlying

(Previously:2.0-5.0) |

US$3.5-5 billion

|

|

Free cash flow at least

(Previously:2.0) |

US$3 billion

|

|

CAPEX guidance 2022-2023

|

US$9-10 billion

|

|

CAPEX guidance 2023-2024

|

US$10-11 billion

|

The profitability during the second quarter was 12.4%, significantly lower compared to the strong Q2 2022. Additionally, Maersk announced that Q2 EBITDA fell to US$2.9 billion and EBIT declined to US$1.6 billion.

Vincent Clerc, CEO of Maersk, commented, “The Q2 result contributed to a strong first half of the year, where we responded to sharp changes in market conditions prompted by destocking and subdued growth environment following the pandemic fuelled years.”

He went on to highlight, “Our decisive actions on cost containment together with our contract portfolio cushioned some of the effects of this market normalisation. Cost focus will continue to play a central role in dealing with a subdued market outlook that we expect to continue until end year.”

Clerc concluded, “While we step this agenda further up, we are unwavering in our transformation and continue to invest in and deliver truly integrated logistics solutions to our customers and amplify their supply chain resilience for the uncertain times ahead.”

Earnings Before Interests, Taxes, Depreciation and Amortization (EBITDA)

| USD million | 2023 Q2 | 2022 Q2 |

|---|---|---|

|

Ocean

|

2,259

|

9,598

|

|

Logistics & Services

|

311

|

337

|

|

Terminals

|

331

|

400

|

|

Towage & Maritime Services

|

59

|

81

|

|

Unallocated activities, eliminations, etc.

|

-55

|

-89

|

|

A.P. Moller – Maersk consolidated

|

2,905

|

10,327

|

Earnings Before Interests and Taxes (EBIT)

| USD million | 2023 Q2 | 2022 Q2 |

|---|---|---|

|

Ocean

|

1,205

|

8,526

|

|

Logistics & Services

|

115

|

234

|

|

Terminals

|

269

|

316

|

|

Towage & Maritime Services

|

71

|

16

|

|

Unallocated activities, eliminations, etc.

|

-53

|

-104

|

|

A.P. Moller – Maersk consolidated

|

1,607

|

8,988

|

Source: Container News