Ocean rates continue to ease post-Lunar New Year: Freightos analysis

13/03/2024![]()

Hostilities in the Red Sea intensified last week, and included the first seafarer casualties. But with most container traffic already avoiding the Suez Canal, demand easing as the market enters its slow season, and operations settling into a new routine, rates continued to ease across the major trade lanes.

Asia – North America ocean rates are down 10% from their peak, with Asia – North Europe prices 22% lower and Asia – Mediterranean rates 34% below their high in late January. Ocean logistics out of India had been the hardest hit by the Red Sea disruption, but even on this lane rates are beginning to decline and some carriers are postponing surcharges or increases that had been planned for March.

Ocean rates – Freightos Baltic Index:

- Asia-US West Coast prices (FBX01 Weekly) fell 7% to US$4,419/FEU.

- Asia-US East Coast prices (FBX03 Weekly) fell 8% to US$6,107/FEU.

- Asia-North Europe prices (FBX11 Weekly) fell 4% to US$4,313/FEU.

- Asia-Mediterranean prices (FBX13 Weekly) fell 10% to US$4,479/FEU.

Last week at TPM, Sea Intelligence’s Alan Murphy estimated that rates should settle around 1.5 to 2X above the long-term average, which would mean prices still have a way to go to their new floor as Asia – North America West Coast and North Europe prices are more than triple 2019 levels and East Coast and Mediterranean rates are still more than double.

The latest National Retail Federation report shows that North American ocean import volumes in January were 8% higher than last year and February imports were 23% higher than a year ago. H1 totals are projected to be 8% higher than in 2019, suggesting modest growth and also showing that container volumes continue to flow despite the Red Sea complications.

As ocean expert Lars Jensen recently put it, the diversions are really a challenge, not a crisis, and the extra vessels needed to service the longer routes are absorbing extra capacity and leading to a balanced market.

But when Red Sea traffic resumes we can expect overcapacity to return, rates to fall and blank sailings to increase, though not all observers agree on how significant overcapacity will prove to be.

In air cargo, Red Sea disruptions to ocean freight have led to some shift to air and increased volumes in February. And though there were reports of congestion at hubs like Bangkok and Dubai in early March, rates on most lanes are subsiding, with China – North America Freightos Air Index rates at US$4/kg last week and China – Europe rates at US$3/kg.

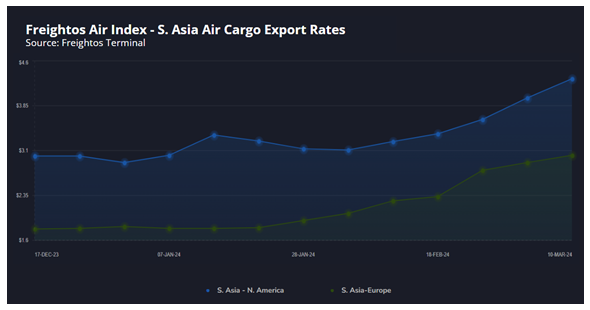

Air rates out of South Asia, however, where as mentioned above, ocean disruptions were the most severe, have continued to climb through last week. South Asia – North America rates have increased 43% since mid-December to US$4.30/kg and to Europe prices have climbed 67% to US$3.02/kg.

Air rates – Freightos Air index

- China – North America weekly prices fell 20% to US$3.97/kg

- China – North Europe weekly prices increased 35% to US$2.97/kg.

- North Europe – North America weekly increased 4% to US$2.08/kg.

The article was written by Judah Levine, head of research at Freightos, a global freight booking and payment platform.